Waterfalling, Header Bidding, and the Evolution of Programmatic Auction Dynamics

In the early days of online advertising, ad space was purchased much like print inventory — directly from publishers at a set price, typically on a cost-per-mille (CPM) basis. During the late 1990s and early 2000s, a wave of new advertising-technology platforms — ad networks chief among them — emerged to help advertisers reach audiences across more sites and give publishers a broader channel for selling inventory.

The real inflection point came in 2007/2008 with the introduction of real-time bidding (RTB). RTB changed the industry in two significant ways.

First, it allowed advertisers to purchase media on an impression-by-impression basis, enabling them to reach specific users across many different websites rather than reaching many users on a single site.

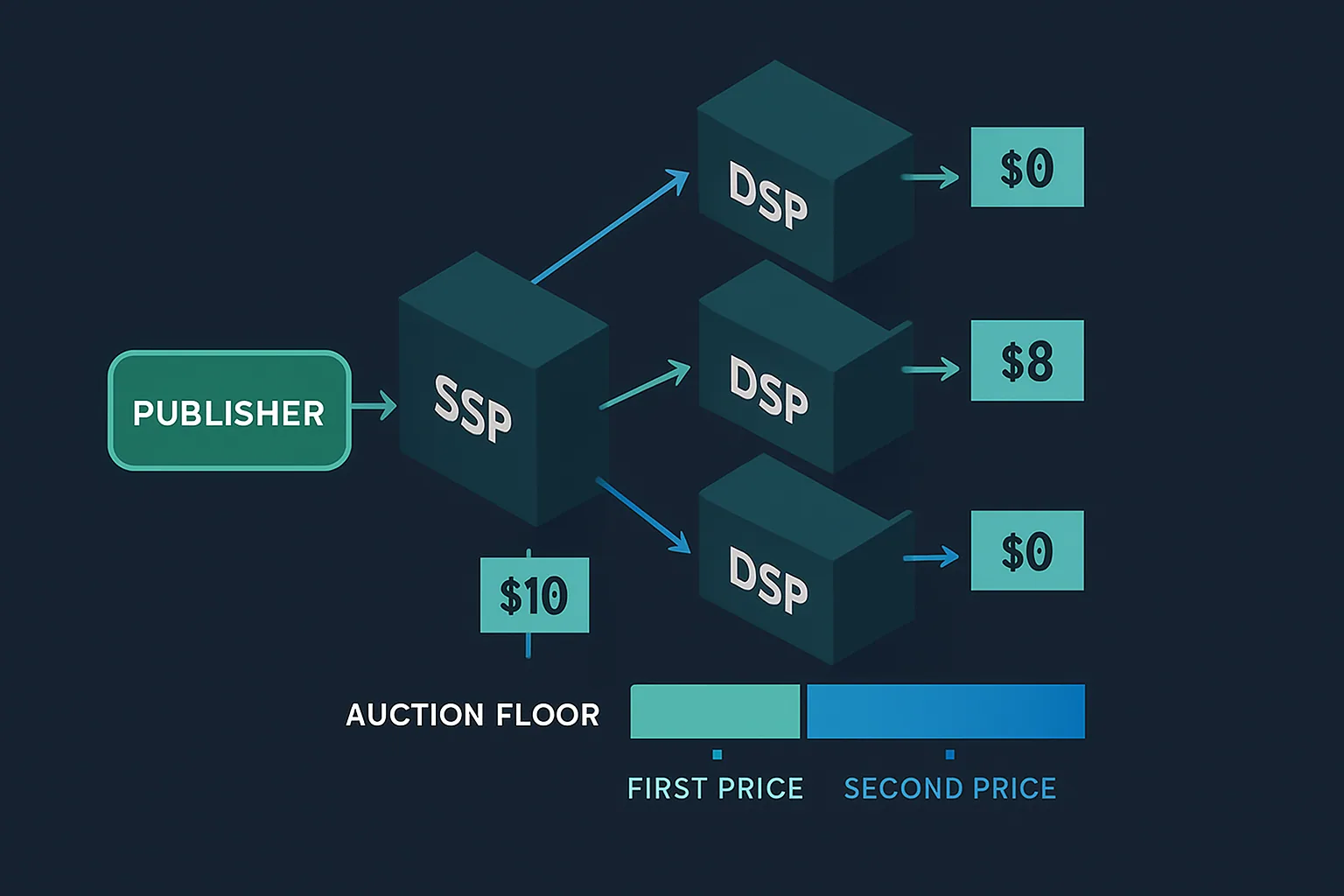

Second, it introduced a new commercial mechanism: the second-price auction. Programmatic ad buying embraced this model and relied on it for years. Under second-price rules, bidders are incentivized to bid their true value because the winner pays only the second-highest bid plus $0.01 — not their actual bid.

More recently, however, a combination of transparency pressures and revenue optimization tactics has driven a steady shift toward auction models that more closely resemble first-price auctions. The turn by ad exchanges and SSPs toward first-price mechanics stems largely from increased pressure to reduce undisclosed take rates — the fees applied to what is known as the "consumer surplus," or the difference between the winning bid and the clearing price — which have historically not been visible to publishers.

This guide explains how the programmatic auction ecosystem evolved from waterfalling through header bidding to today's hybrid auction models, and what the trade-offs of each approach look like in practice.

From Waterfall to Header Bidding

Publishers are working to recover revenue lost to reductions in second-price programmatic auctions. This is part of why SSPs and ad exchanges have increasingly layered in combinations of soft and hard price floors — effectively engineering hybrid first-and-second-price auctions. Simultaneously, the industry has moved toward newer structural approaches that address yield and fill-rate problems that older methods could not solve.

Waterfalling

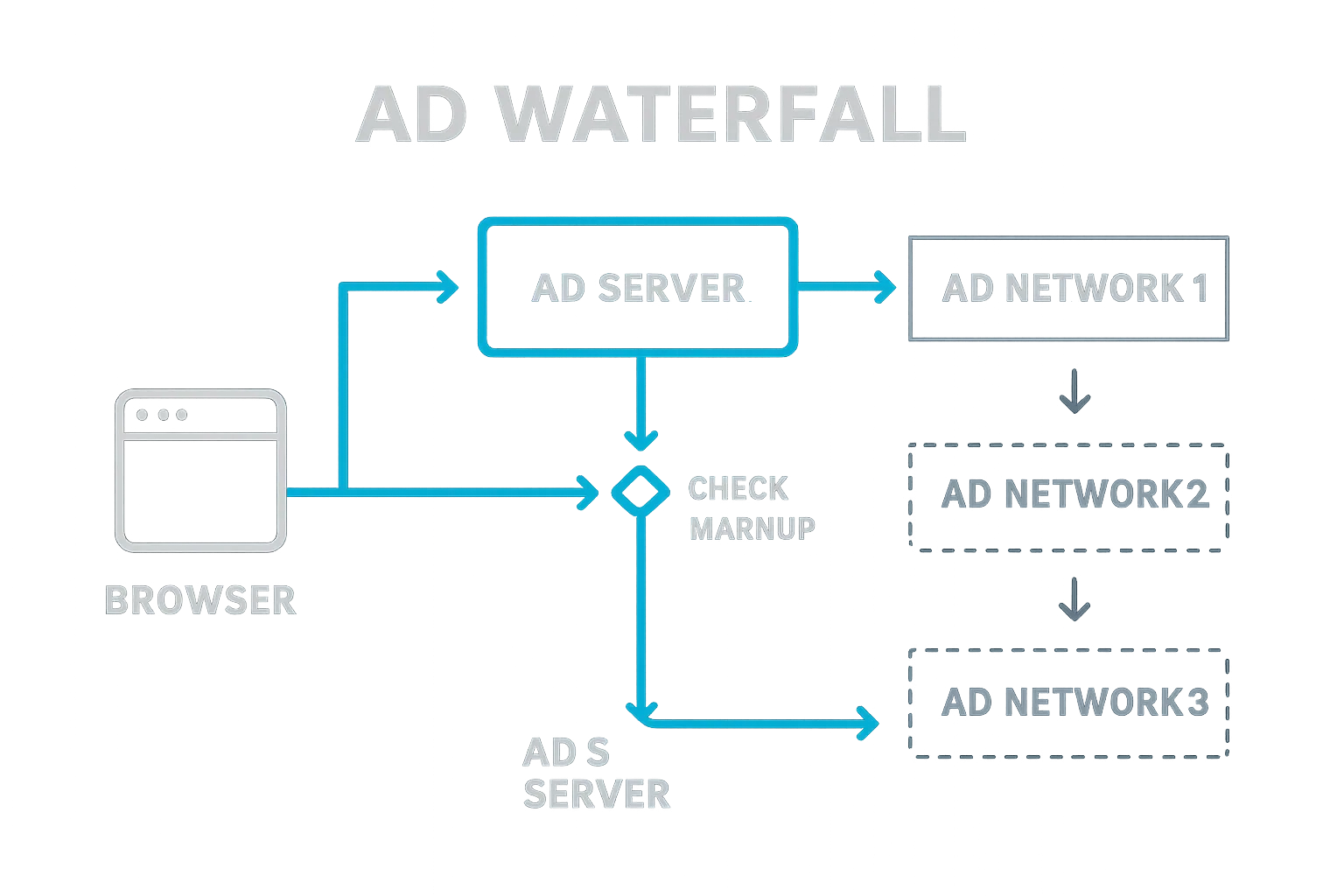

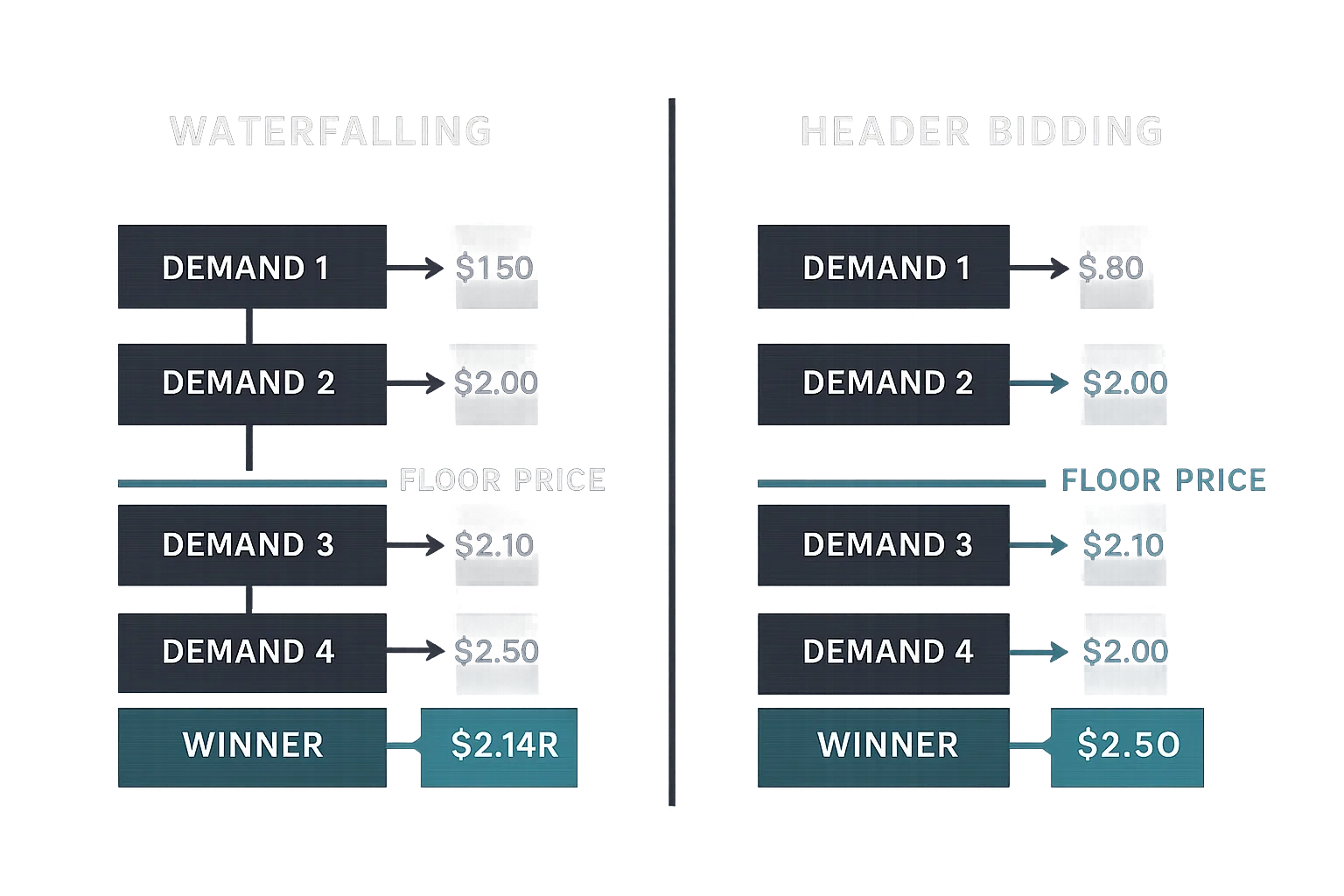

Before header bidding existed, publishers relied entirely on waterfall auctions. Waterfalling — also called a daisy chain or waterfall tags — is a process that sells publisher inventory sequentially, activating one demand source at a time.

In a waterfall setup, each new impression is first processed through the publisher's ad server to match it against direct campaigns. If no eligible direct campaign is found, the impression is passed to the next partner in line — typically an ad network or SSP — which attempts to fill it. If that partner fails, the impression is passed back to the ad server and on to the next partner in the chain.

The order of the waterfall is typically determined by average historical yield: the average revenue that each demand source has historically generated for the publisher. Once an impression is filled by any source, all other demand sources in the waterfall are bypassed — meaning higher bids that could have been available elsewhere are never considered.

Problems With Waterfalling

Publishers used waterfalling to prioritize partners from highest to lowest average payer. While logically structured, this approach actively suppressed competition: partners lower in the waterfall rarely had a chance to bid, even if they would have paid more for a specific impression.

The core problems with waterfalling break down as follows:

Yield risk: The ad server selects which partner to call based on average historical yield, but averages are poor predictors of any individual impression's real-time value. Publishers were effectively managing inventory based on assumptions rather than live market data. The result: the highest bid for a given impression was often never seen, because not every partner had the opportunity to participate.

Fill risk: Even when the ad server identified the highest average-yield partner, that partner might not actually fill the impression. That failure wasted a call and forced publishers to maintain contingency plans — calling a second partner, or passing the impression back to the ad server for another round of decisioning. Knowing whether an exchange could fill an impression before calling it was critical, and waterfalling provided no way to do that.

Pass-back pain: Managing complex contingency chains — constantly optimizing, analyzing, and updating historical yield rates — placed an enormous operational burden on AdOps teams. Logging into multiple platforms, de-duplicating pass-back impressions, and manually updating partner rankings is significant manual labour for a process that is supposed to be fully automated.

Compounding problems: Fill risk and yield risk are linked. Because publishers can't identify the best-value impression in advance, they set conservative floors that exclude capable partners — which then leads to more fill failures. Header bidding was developed specifically to break this cycle.

Header Bidding

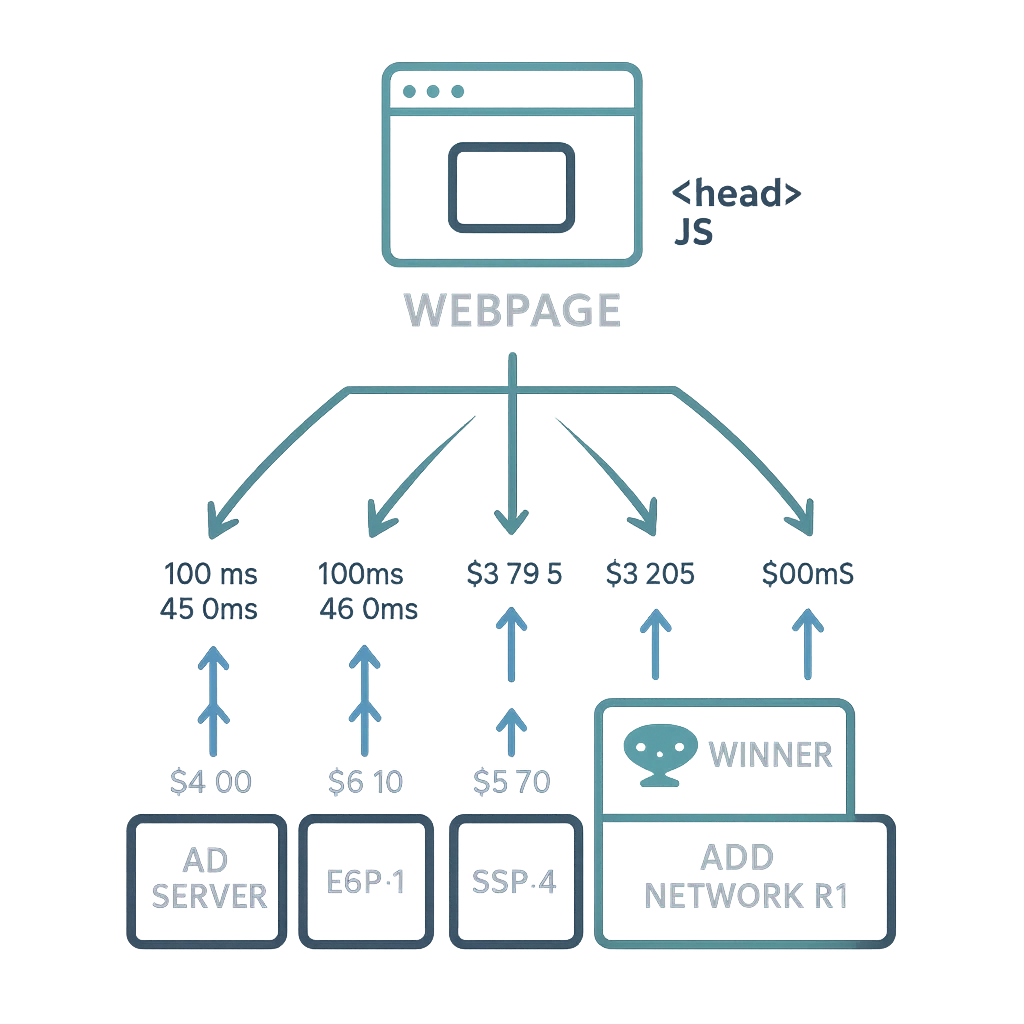

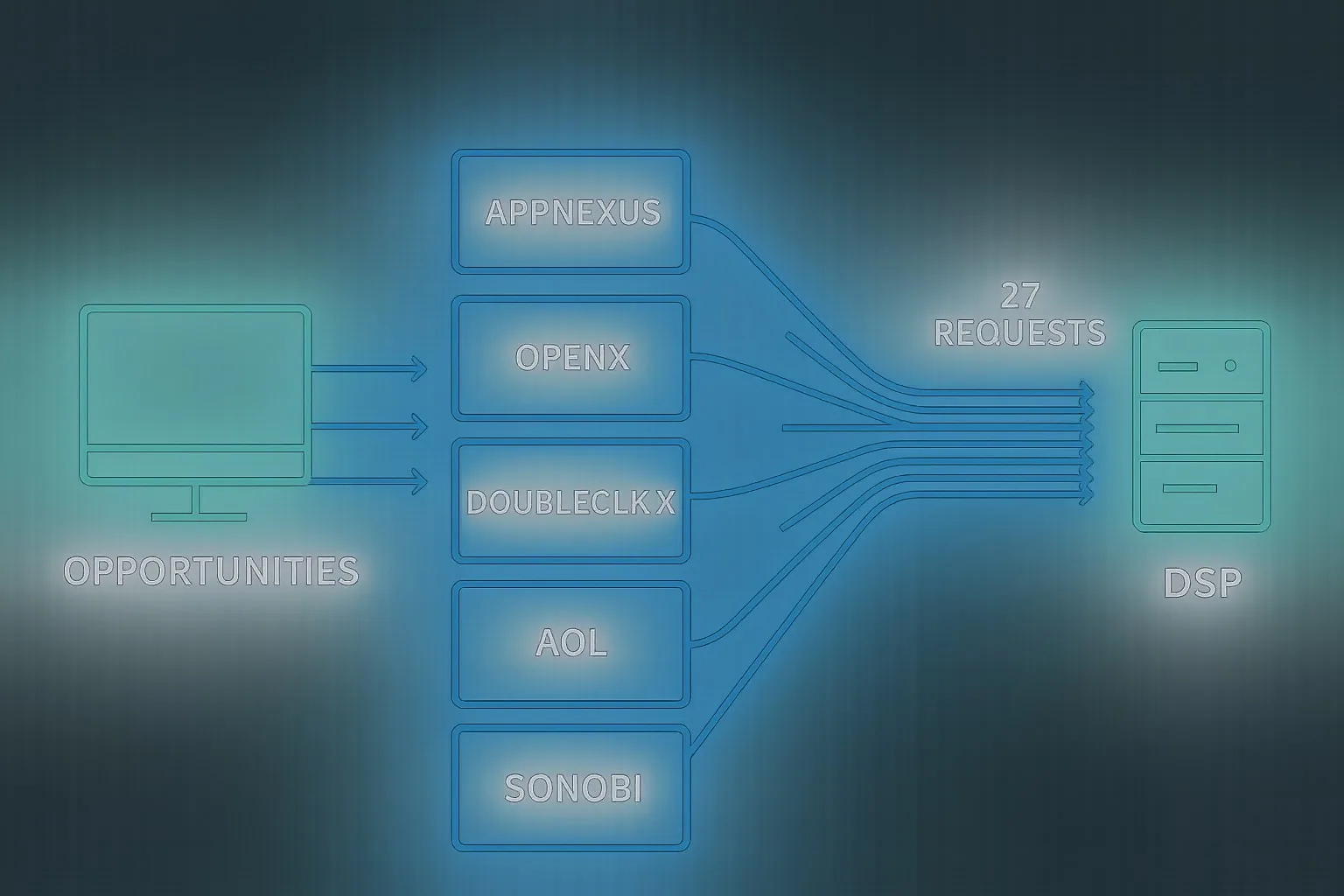

Header bidding is the practice of soliciting bids from multiple demand sources before the primary ad call is made to the publisher's ad server, and then feeding those bids into the ad decisioning process. It works by embedding a piece of JavaScript in the <head> of a web page that fires simultaneous bid requests to multiple SSPs and exchanges — hence the name "header bidding."

Header bidding was introduced to give publishers access to genuine market-wide competition for each impression. Key benefits include:

Higher Yields

Header bidding lets publishers see how much each demand source will pay for an impression before the final serving decision is made. Instead of relying on average historical yield, publishers see real-time bids from all integrated demand sources simultaneously. The highest-paying source wins the impression.

Higher Fill Rates

Higher yields and higher fill rates are closely connected. With header bidding, the publisher knows in advance whether each SSP or exchange will actually deliver on its bid. No impressions are wasted on partners that cannot fill. By eliminating fill risk, the publisher can retire complex sequential waterfall chains: each SSP bids on what it will actually fill at 100%, so there is no need for pass-back logic or daisy-chain management.

Header bidding offers fair competition between guaranteed direct-sold campaigns and RTB demand, and does so without sacrificing the impression to test the market.

Problems With Header Bidding

Header bidding is a substantial improvement over waterfalling, but it introduces its own inefficiencies.

Privacy concerns: Because header-bidding requests are sent simultaneously, every bidder gains access to data from all users who are served impressions from that auction. Publishers can integrate a dozen or more header-bidding partners, and some exchanges allow DSPs to receive bid requests essentially as passive listeners — absorbing data without ever spending. As the number of bidding partners grows, so does the risk of user data reaching those partners' customers and propagating further.

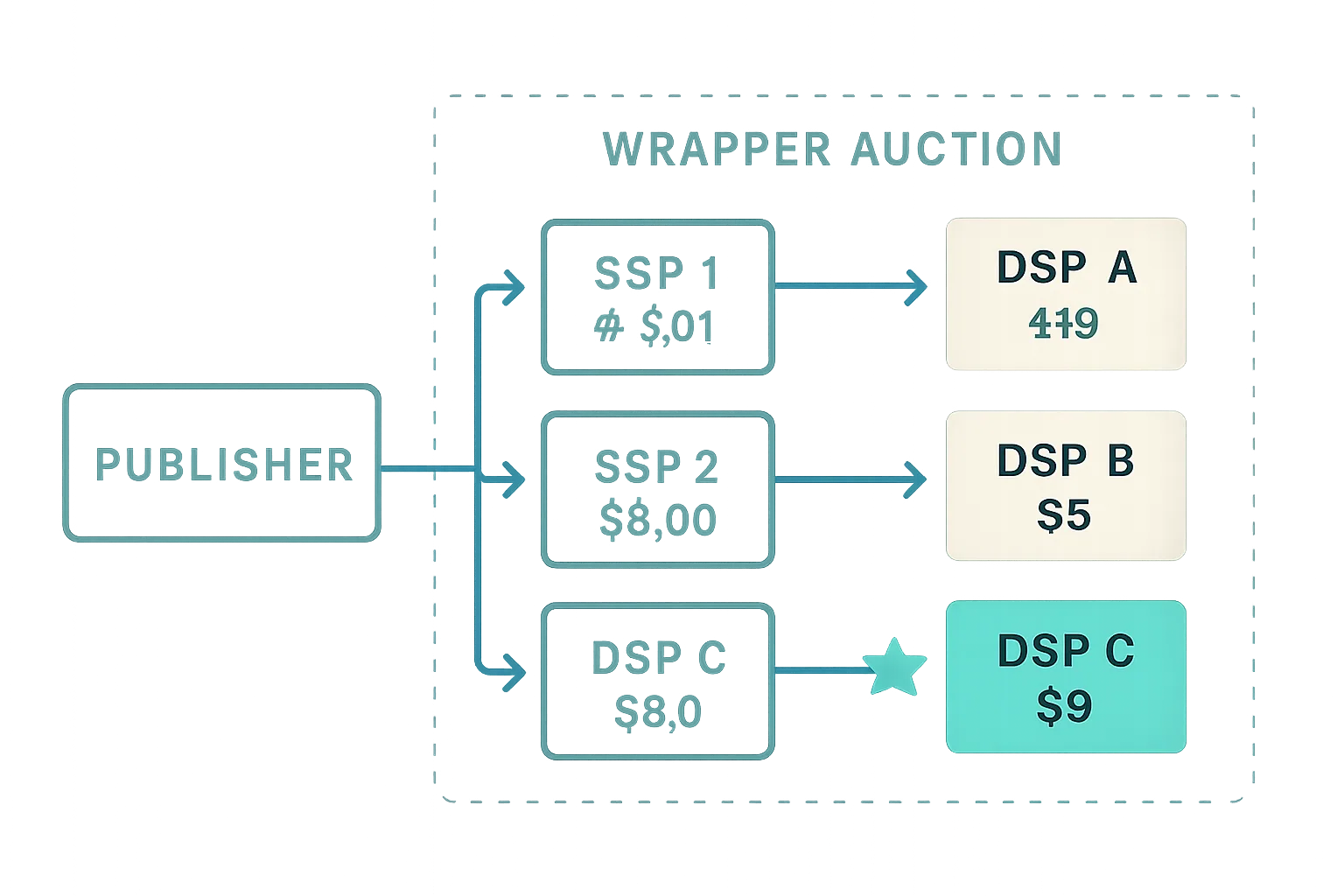

Many requests, one DSP: Header-bidding requests go out to multiple SSPs, but many of those SSPs forward the requests to the same underlying DSPs — creating redundant, duplicated auctions and added latency with no incremental value.

Inefficiencies and unpredictability of sequential auctions: The current header-bidding model involves sequential second-price auctions — first at the SSP level, then at the header-bidding wrapper level. This layering is intended to maximize fill, but it produces unpredictable outcomes. The highest bidder is no longer guaranteed to win, and publishers are not guaranteed to receive the maximum price buyers were willing to pay.

New Auction Dynamics

Header bidding improved on the waterfall model, but sequential auction structures introduced new problems. To understand how, consider the following example of a typical header-bidding flow:

- A user loads a web page.

- The header-bidding wrapper sends simultaneous requests to multiple SSPs/ad exchanges.

- Each SSP/ad exchange broadcasts the bid request to connected DSPs.

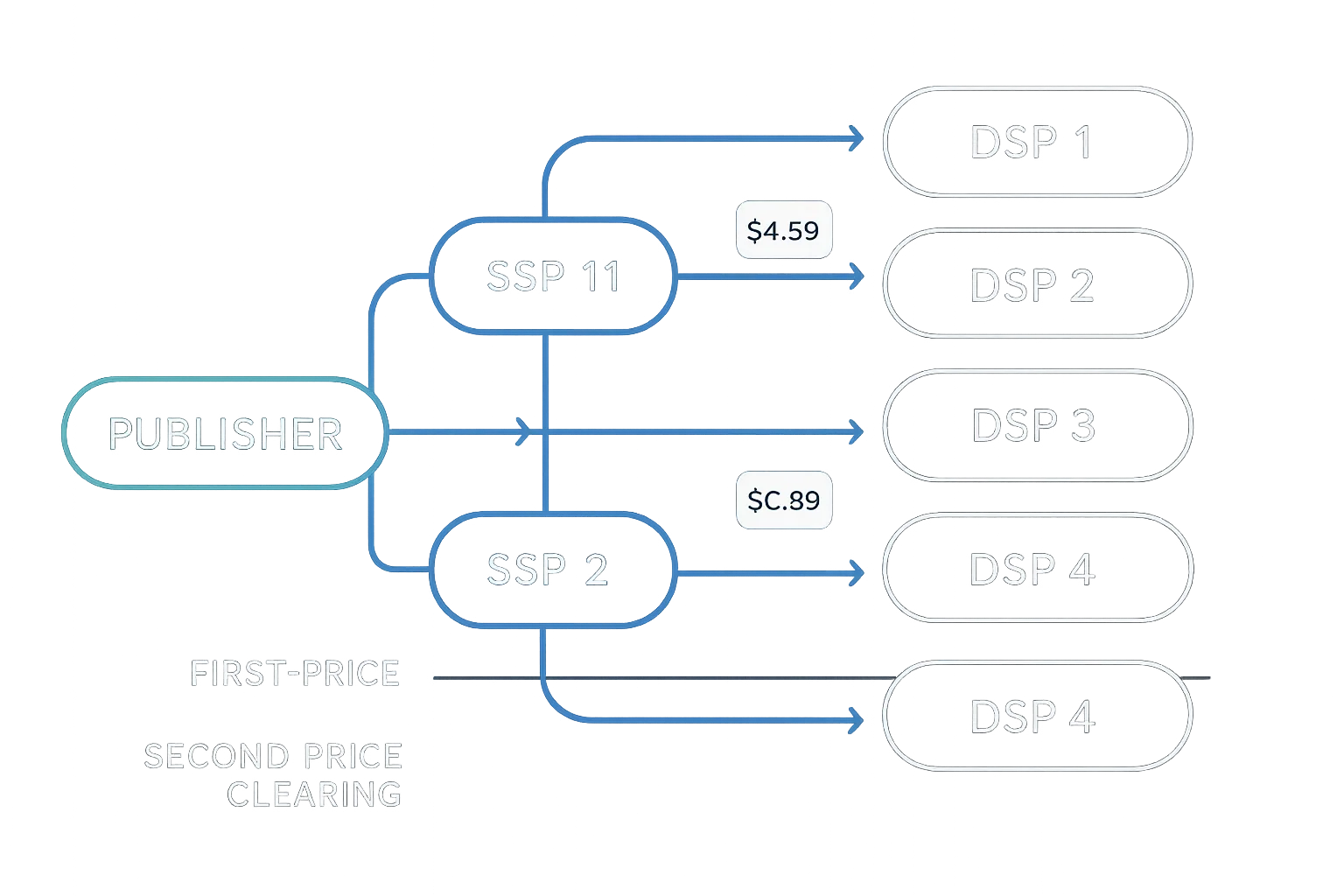

- DSPs respond with bids representing the maximum CPM their matched campaigns will pay — for example, $10, $5, $8, and $6.

- Each SSP runs a second-price auction internally. If one SSP received bids of $10 and $5, the clearing price is $5.01 CPM.

- The SSP returns its clearing price ($5.01) to the header-bidding wrapper.

- The wrapper runs a first-price auction among all returned clearing prices and serves the impression to the winner.

The inefficiency is visible here: a buyer willing to pay $10 exists, but because that SSP's second-price auction cleared at $5.01 — due to limited competition within that SSP — it may lose to a different SSP whose clearing price happened to be higher. The publisher never receives the $10 that was on the table.

Arguments for First-Price Auctions

Multi-level sequential auctions can heavily favour bidders over sellers. When a second-price auction runs at the SSP level and a first-price auction runs at the wrapper level, lower bids can end up winning simply because there was less competition within a specific SSP. Publishers, trying to protect yield, introduced soft and hard price floors — but these tactics turn second-price auctions into quasi-first-price auctions while simultaneously obscuring the rules of the game for buyers.

The second-price auction model stops being truthful when it is not the final auction in a chain. In sequential settings, limited competition for certain impressions leads to dynamic pricing through floor optimizations, which amounts to a form of price discrimination. DSPs and advertisers have pushed back against these tactics, calling for SSPs to stop cascading auctions, the aggregation of header and DSP bids, and floor manipulations that damage trust in the marketplace.

Interestingly, these concerns were articulated as early as 2012 by Adam Drake in his post on Real-Time Bidding, First and Second-Price Auctions, and Transparency — well before the current wave of first-price adoption.

The case for first-price auctions rests on transparency. They eliminate unclear flooring tactics, cascading auction structures, and the ambiguity about what a buyer will actually pay. The rules are simple: you bid what you want to pay, and if you win, you pay that amount.

Arguments Against First-Price Auctions

First-price auctions rarely favour the bidder. There is no consumer surplus — the winner pays their full bid, with no reduction. The risk of overbidding falls entirely on the buyer.

In a first-price auction, all bids are sealed. Bidders don't know what competitors are submitting. Successful participation requires a reasonably accurate estimate of an impression's value and an informed guess about what others might bid. The rational response is to bid conservatively — somewhat below true value — to avoid overpaying. Getting that calibration right requires meaningful data and ongoing bid-shading strategies, which adds complexity on the buy side.

Industry Recommendations for Implementation

Publishers consistently seek auction structures that maximize yield and fill rates, and the industry has produced a number of concrete proposals for how to rationalize the layered auction problem. Most modern implementations are built on the OpenRTB protocol, which provides specific fields to communicate auction type in bid requests — allowing SSPs to signal to DSPs whether a given auction is first- or second-price.

Dynamic Switching Between First- and Second-Price Auctions

OpenX has been among the most active proponents of first-price auctions, enabling first-price mechanics on its platform and explaining the rationale to demand partners. The goal is to improve the competitiveness of DSP bids when those bids flow into subsequent header-bidding auctions.

OpenX recommends that first-price auctions be used for all non-final auctions — for example, when the final auction occurs at the header-bidding wrapper level. In that context, it is in the demand partner's interest to submit a first-price bid, since it increases the likelihood of surviving to the final stage. When OpenX itself runs the final auction, a second-price model is used as normal.

Second-Price Auction Administered Only by the Publisher

PubMatic has proposed an alternative integration method: SSPs pass their first-price bids directly to the publisher, who then runs a single second-price auction to determine the winner and set the clearing price. This is the inverse of the current standard, where SSPs return a second-price clearing price to the wrapper.

Under this model, publishers and technology platforms can focus on creating value and improving overall industry economics rather than gaming multi-level auction structures. Giving publishers direct control over auction mechanics enables better control of revenue streams, reduces inefficiencies, and supports more meaningful use of segmentation, data fidelity, addressability, and viewability signals.

Where Things Stand

Programmatic ad buying has moved through a clear arc — from manual waterfalling, through header bidding, to increasingly sophisticated first- and second-price auction configurations. Auction mechanics have never been perfectly fair or transparent, but the current period of structural reform is pushing the ecosystem closer to a level playing field.

The direction of travel is clear: sequential auctions that obscure true market prices and favour buyers at the expense of publishers are being replaced by structures with simpler, more transparent rules. Whether that means pure first-price auctions, hybrid publisher-controlled models, or dynamic switching between types will depend on how SSPs, DSPs, and publishers negotiate the trade-offs — but the trend toward greater clarity in what buyers pay and what sellers receive is unlikely to reverse.